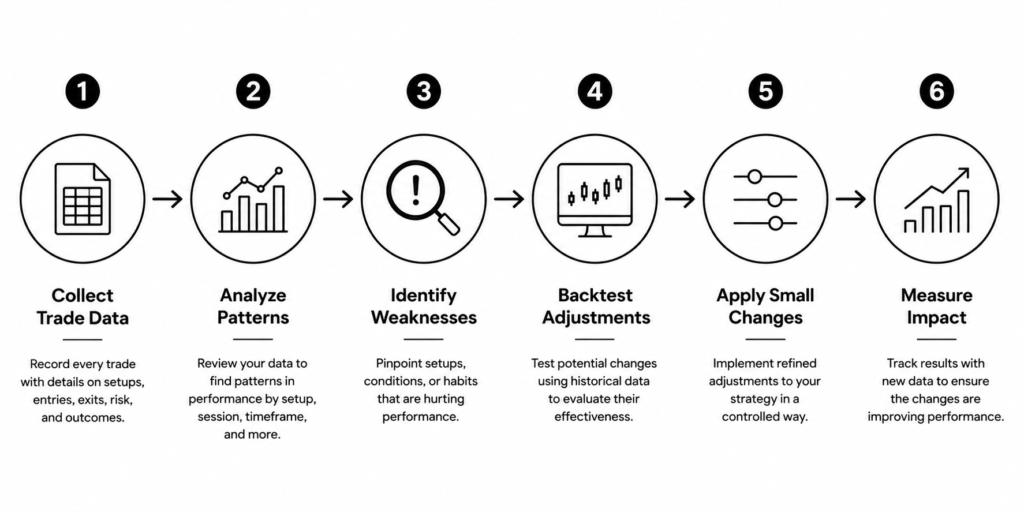

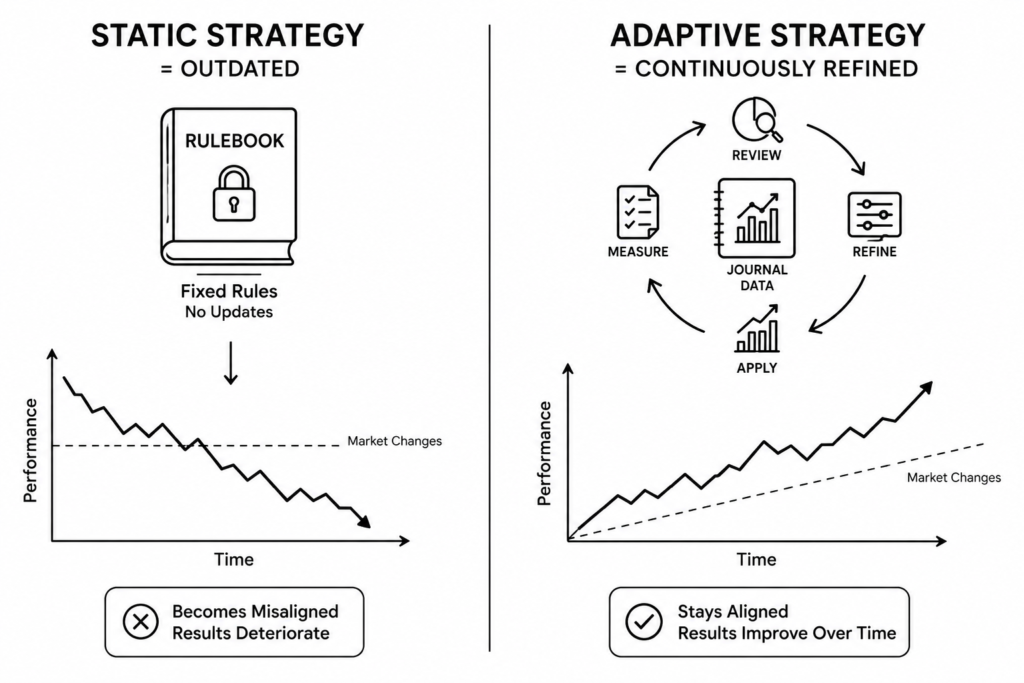

Most traders write their trading strategy once and then treat it as a fixed document that evolves only when results become bad enough to force a reaction. They add a rule after a particularly painful loss, remove a setup after a frustrating streak, and otherwise leave the strategy largely unchanged from one month to the next regardless of what their trading data is showing them. The most consistently profitable traders operate differently. They treat their strategy not as a finished document but as a living system that is continuously tested against real performance data and refined based on what that data reveals. The strategy they trade today is not the same strategy they traded six months ago, and the difference is not that they found a better system. It is that they used their journal data to make it better themselves.

The gap between these two approaches is not talent, market knowledge, or access to better information. It is the disciplined and structured use of journal data to make specific, evidence-based changes to how they trade. Every trader who journals consistently is sitting on the data needed to refine their strategy in meaningful and measurable ways. Most of them never act on it because they do not have a clear process for translating what the data shows into concrete modifications to their trading plan.

This guide provides exactly that process. It covers how to identify which setups to cut, scale, or refine based on performance data, how to adjust position sizing and session exposure using journal insights, how to validate proposed changes through backtesting before applying them live, and how to implement modifications in a controlled way that isolates their impact and allows their effect to be measured. If you have not yet built a structured review process for your journal data, start with our Trading Self-Analysis Guide, which covers the weekly, monthly, and quarterly review framework that generates the insights this guide is built around. For traders who are earlier in their journaling journey, our Complete Trading Journal Guide covers everything needed to set up an effective journal from scratch. This guide picks up where both of those leave off, at the point where the data is in front of you and the question is what to do with it.

Key Takeaways

This guide covers how to translate trading journal data into specific, evidence-based strategy modifications, giving you a practical process for refining your setups, sizing, session exposure, and trading plan on a continuous basis.

- The most consistently profitable traders treat their strategy as a living system that evolves based on journal data rather than a fixed document that only changes after significant losses.

- Strategy refinement requires a minimum sample size before any modification is justified, and changes made on insufficient data are guesses rather than evidence-based decisions.

- Journal data should drive specific and separate decisions about which setups to cut, which to scale, and which to refine through rule modification rather than elimination.

- Position sizing, session exposure, and instrument selection should all be adjusted based on what the data shows rather than on intuition or habit.

- Every strategy modification identified through journal review should be validated through backtesting before being applied at full scale in live trading.

- Strategy refinement works best when embedded into a regular review cycle as a recurring process rather than conducted reactively after a period of poor performance.

Why Your Trading Strategy Should Never Be Static

A trading strategy is not a discovery. It is not a fixed truth about how markets work that, once found, can be applied indefinitely without modification. It is a set of rules that reflects a trader’s current understanding of where their edge exists under current market conditions, and both of those things change over time in ways that make a static strategy progressively less aligned with the reality it was designed to exploit.

Markets evolve continuously. Volatility regimes shift. Liquidity patterns change. The behaviour of participants in a given market at a given time is different from their behaviour six months earlier or six months later, and a strategy built around specific market conditions that no longer exist will produce deteriorating results not because the trader has gotten worse but because the environment the strategy was calibrated for has moved on. This is not a theoretical risk. It is a practical reality that affects every trader who operates with a fixed rulebook long enough for the market conditions underlying that rulebook to change meaningfully.

A trader’s edge also shifts over time independently of market conditions. As a trader gains experience, their ability to read certain setups improves while their relationship with others changes in ways that affect execution quality. A setup that was profitable in the early stages of a trading career because it matched a trader’s natural decision-making style may become less profitable as the trader develops new tendencies that introduce friction into how that setup is executed. A setup that was marginal early on may become significantly more profitable as the trader develops the patience and discipline that setup requires. These shifts are real and they show up in the data, but they are invisible to a trader who is not looking at setup-specific performance over time.

Journal data is the only reliable source of real-time feedback on whether a strategy is still working and in which specific areas it needs to change. No external source of market analysis, no trading community, and no general advice about strategy development can tell a trader what their specific edge looks like right now across their specific setups, sessions, and instruments under current market conditions. Only the trader’s own performance data contains that information, and only a structured review process applied consistently over time surfaces it in a form that is actionable.

The distinction between changing a strategy reactively based on emotion and refining it proactively based on data is critical and worth being explicit about. Reactive strategy changes happen after pain. A significant loss or a bad month triggers a search for something to fix, and changes are made quickly and without sufficient data to justify them because the emotional pressure to do something is stronger than the analytical discipline to wait for a meaningful signal. These changes frequently make things worse because they are responses to recent results rather than to durable patterns in the data, and they introduce new variables into the trading process before the existing variables are properly understood.

Proactive strategy refinement based on data operates on a completely different logic. It is conducted on a fixed schedule regardless of whether recent results have been good or bad. It requires a minimum sample size before any conclusion is drawn. It makes one change at a time and tracks the impact of that change through the ongoing review process before making the next one. It treats the strategy as something to be improved incrementally and continuously rather than overhauled reactively when performance deteriorates. The difference in outcomes between these two approaches over the course of a trading career is not marginal. It is the difference between a strategy that compounds in effectiveness over time and one that oscillates between versions of itself without ever becoming meaningfully better.

How to Refine Your Setup Selection

Setup selection is the most direct lever a trader has over their strategy’s expectancy, and it is the area where journal data produces the clearest and most actionable refinement signals. Most traders trade too many setups simultaneously, spreading attention and risk capital across a range of trade types whose individual performance profiles they have never examined in isolation. Setup-level analysis almost always reveals significant variation that the overall performance statistics were concealing, and acting on that variation is where the most immediate and measurable improvement in strategy performance tends to come from.

Identifying Setups to Cut

The clearest signal that a setup should be cut from a trading plan is negative expectancy across a meaningful sample. Negative expectancy means that the setup is losing money on average across a sufficient number of trades to rule out variance as the primary explanation. When win rate, average R-multiple, and Profit Factor are all reviewed together for a specific setup across a sample of fifty trades or more and the combined picture shows that the setup produces less than one unit of return for every unit of risk taken on average, the setup has a negative expectancy and continuing to trade it is a deliberate choice to lose money at a known rate.

A more subtle but equally important signal is consistently poor R-multiple despite an acceptable win rate. A setup with a 55 percent win rate can still have negative expectancy if the average losing trade is significantly larger than the average winning trade in R-multiple terms. A trader who wins slightly more often than they lose but gives back more on each loss than they make on each win is running a negative expectancy setup regardless of how the win rate looks in isolation. This is one of the most common patterns in retail trading data and one of the most frequently missed because win rate feels like a positive signal even when the R-multiple data is telling a completely different story.

The third signal is a setup that only produces positive results in specific market conditions that are not reliably or frequently present. When setup-specific analysis reveals that the majority of profitable trades in a given setup occurred during a specific volatility regime, a specific trend condition, or a specific time of year, and that the setup performs at break-even or worse outside of those conditions, the setup does not have a durable edge. It has a situational edge that may or may not be present at any given time, which makes it an unreliable component of a trading strategy and a candidate for elimination or significant reduction unless the trader can reliably identify in advance when those specific conditions are present.

Identifying Setups to Scale

The data signals that indicate a setup deserves more focus and potentially more size are the mirror image of the signals that indicate a setup should be cut, but they require an additional layer of analysis before scaling is justified. A setup with consistently positive expectancy across a meaningful sample, a strong average R-multiple relative to its win rate, and performance that holds up across multiple instruments and sessions is a setup that the data is telling a trader to do more of. Most traders underweight these setups because they spread their attention and capital across too many trade types simultaneously and never isolate the performance of their best setups clearly enough to see how much of their overall results they are driving.

Consistently positive expectancy across varying market conditions is the most important signal for scaling because it indicates that the edge is durable rather than situational. A setup that has produced positive expectancy across both trending and ranging conditions, across different volatility regimes, and across multiple months of varying market behaviour is demonstrating a robustness that justifies increased commitment. A setup that has produced positive expectancy only during a specific recent period or only under specific conditions that happened to be present during the review period does not yet have the track record to justify scaling.

Strong R-multiple relative to win rate is the second signal. A setup with a 45 percent win rate and an average R-multiple of 2.5 on winners against 1.0 on losers has a positive expectancy and is a candidate for scaling even though it loses more often than it wins. The R-multiple profile matters more than the win rate in determining whether a setup deserves more capital, and traders who focus primarily on win rate when evaluating which setups to scale will systematically underweight some of their most valuable setups while overweighting setups that feel more comfortable because they win more frequently.

Performance across multiple instruments and sessions is the third signal and it is the one that most clearly indicates a setup’s edge is genuine rather than an artefact of a specific market or time period. A setup that produces positive expectancy on three different instruments across two different sessions is showing something about the nature of the trade type itself rather than about the specific conditions of a single market during a specific period. That breadth of positive performance is a strong signal that increasing focus and size on that setup is justified by the data.

Identifying Setups to Refine

Between the setups that should be cut and the setups that should be scaled sits a third category that is often the most instructive for strategy development. These are setups that show genuine promise in the data, a positive or near-positive expectancy, a reasonable R-multiple profile, and evidence of a real edge in certain conditions, but that also have specific and identifiable weaknesses that are dragging their performance below what the underlying edge should produce. These setups are candidates for rule modification rather than elimination, and the journal data typically contains enough information to identify exactly which rules need to change.

Adjusting entry criteria is the most common refinement for this category of setup. When holding time analysis and trade outcome data reveal that a significant proportion of the losing trades in a setup were entered before the setup was fully formed, tightening the entry criteria to require additional confirmation before a position is opened can improve the setup’s expectancy without changing its fundamental logic. The data will show this pattern as a cluster of losing trades with shorter than average holding times that were stopped out quickly after entry, which indicates that the entry was taken too early and that waiting for additional confirmation would have either produced a better entry or kept the trader out of the trade entirely.

Tightening or widening stop placement is the second refinement lever. When the data shows that a high proportion of losing trades in a specific setup were stopped out and then moved in the intended direction, the stop placement rule may be too tight relative to the normal price action of that setup. Widening the stop, and adjusting position size accordingly to maintain the same risk per trade, may improve the setup’s win rate without meaningfully changing the average R-multiple on losing trades. When the data shows the opposite pattern, losers that ran significantly beyond the stop before reversing, tightening the stop and accepting a lower win rate in exchange for a better R-multiple profile may improve overall expectancy.

Modifying exit rules based on holding time analysis is the third refinement lever and addresses one of the most common patterns in retail trading data. When the analysis shows that winning trades in a specific setup are being closed significantly earlier than their average maximum favourable excursion, the exit rule may be cutting winners short in a way that is suppressing the setup’s average R-multiple below what the underlying edge would produce if exits were managed differently. Extending the exit rule, whether through a wider target, a trailing stop, or a time-based exit rather than a fixed target, and then tracking the impact of that change through the ongoing review process, addresses this pattern in a specific and measurable way rather than through a general intention to hold winners longer.

How to Adjust Position Sizing Based on Journal Data

Position sizing is the most direct expression of how much confidence a trader’s data justifies in any given setup, session, or market condition, and it is one of the most underused levers in strategy refinement. Most traders apply a uniform position size across all trades regardless of what their journal data shows about the variance and consistency of different setups, the performance variation across different sessions, or the impact of their psychological state on execution quality. Uniform sizing treats all trades as equally deserving of the same capital allocation, which is rarely what the data supports and which leaves significant performance improvement on the table for traders who have the data to size more intelligently but have not yet acted on it.

The first sizing adjustment that journal data supports is reducing size on setups with high variance or inconsistent results. High variance in a setup’s results, meaning a wide distribution of outcomes across trades rather than a consistent cluster around the average, indicates that the setup is less predictable than the average statistics suggest. A setup with a positive average R-multiple but a very wide range of individual trade outcomes carries more risk per trade than its average suggests because the actual result of any individual trade is less certain. Reducing size on high-variance setups limits the damage that outlier losing trades in those setups can produce while the trader continues to gather data and assess whether the variance is a permanent feature of the setup or a temporary reflection of specific market conditions.

The second adjustment is increasing size on setups with consistently strong risk-adjusted returns across a meaningful sample. When a setup has demonstrated positive expectancy across fifty or more trades, a strong and consistent average R-multiple, and performance that holds up across varying market conditions, the data is providing a clear argument for allocating more capital to that setup. Most traders who have identified their best setup through journal analysis are still sizing it the same as their worst setup because they have not translated the insight the data provides into a concrete sizing rule. Increasing size on the highest-conviction setups, defined by data rather than by feeling, is one of the most direct ways to improve overall strategy performance without changing anything about how those setups are identified or executed.

The third adjustment is applying session-based sizing rules where data shows performance varies significantly by time of day. When monthly and quarterly reviews consistently show that a trader performs significantly better during one session than another, the logical sizing response is to trade larger during the high-performance session and smaller during the lower-performance session rather than applying the same size across both. This does not require eliminating the underperforming session entirely, though that may be the right conclusion in cases where the underperformance is severe and consistent. It requires acknowledging what the data shows about where the edge is strongest and allocating capital in proportion to that signal. A trader who sizes at full capacity during their worst session and full capacity during their best session is ignoring information their journal has already provided about where their capital is best deployed.

The fourth and most psychologically nuanced adjustment is using mental state data to implement dynamic sizing rules that reduce exposure during identified high-risk psychological conditions. When journal data reveals a consistent correlation between specific mental state conditions and deteriorating performance, the appropriate response is not simply to be aware of that correlation but to build it into the sizing rules in a way that limits the damage those conditions produce automatically rather than relying on in-the-moment discipline to override them. A rule that reduces position size by fifty percent on any day where stress is logged above a defined threshold, or on any day following a loss above a defined size, or during any session where more than a defined number of consecutive losses have occurred, removes the decision about whether to reduce size from the emotional environment where that decision is hardest to make correctly and places it in the rule system where it can be applied consistently regardless of how the trader feels in the moment.

The practical process for implementing data-driven sizing adjustments is straightforward but requires discipline in execution. Define the sizing rules in writing as part of the trading plan rather than as informal intentions. Specify exactly which setups, sessions, or conditions trigger each sizing rule and by how much size is adjusted in each case. Track the impact of the sizing changes through the ongoing journal review process by comparing risk-adjusted performance before and after the adjustments across a sufficient sample. And resist the temptation to override the sizing rules based on how a specific trade feels in the moment, because the rules are based on what the data shows across hundreds of trades and the feeling in the moment is based on what one trade looks like right now, which is a far less reliable source of information about the right sizing decision.

How to Adjust Session and Instrument Exposure

The question of when to trade and what to trade is treated by most traders as a matter of preference, availability, and habit rather than as a data-driven decision that the journal is already equipped to answer. Session and instrument exposure are two of the most significant variables in a trading strategy, and they are two of the variables that journal data addresses most directly and most clearly once the analysis is conducted at the right level of granularity. Adjusting exposure based on what the data shows rather than on what feels familiar is one of the most impactful and most underutilised forms of strategy refinement available to retail traders.

The starting point is identifying sessions that are consistently underperforming across a meaningful sample. Consistent underperformance means negative or significantly below-average results across a minimum of fifty trades during that session spanning a variety of market conditions and time periods rather than a recent run of poor results during a specific regime that may not be representative. When the data meets that threshold and shows that a specific session is producing negative expectancy or a risk-adjusted return significantly below the trader’s overall average, the argument for continuing to trade that session at full size is difficult to make on any basis other than habit or the unwillingness to accept what the data is showing.

The appropriate response to consistently underperforming session data depends on the severity and consistency of the underperformance. A session that is marginally below the overall average across a moderately sized sample warrants monitoring and reduced size rather than elimination. A session that is producing negative expectancy consistently across a large sample and across varying market conditions warrants elimination from the trading schedule until there is a specific and data-supported reason to believe the conditions driving the underperformance have changed. The difference between these two responses is not the trader’s comfort level with trading fewer hours. It is what the data specifically shows about the severity and durability of the underperformance.

Concentrating activity in sessions where data shows a genuine and durable edge is the positive counterpart to session elimination and is equally important as a refinement decision. When journal data clearly identifies one or two sessions as the primary drivers of overall profitability, increasing focus, preparation, and capital allocation during those sessions produces a direct improvement in strategy performance without requiring any change to the setups being traded or the rules governing them. A trader who identifies through journal analysis that eighty percent of their profitable trades occur during a specific two-hour window and responds by treating that window as the primary trading session and all other sessions as secondary or optional has made a significant strategy improvement based entirely on information their journal already contained.

Instrument-specific exposure adjustments follow the same logic but require an additional consideration that session adjustments do not. Markets and instruments have different characteristics at different times, and a trader’s edge on a specific instrument may be genuine but temporarily suppressed by market conditions rather than permanently absent. Before cutting exposure to an instrument based on a period of underperformance, it is worth assessing whether the underperformance coincides with a specific market condition on that instrument such as unusually low volatility, a trending regime on an instrument that produces better results in ranging conditions, or a liquidity change that has affected the quality of price action during the review period. If the underperformance is clearly condition-specific rather than consistent across varying environments, reducing size during those conditions rather than cutting the instrument entirely is the more precise and more data-supported response.

When the data shows no consistent positive expectancy on a specific instrument across a meaningful sample and across varying market conditions, the case for cutting or significantly reducing exposure to that instrument is straightforward. Traders maintain exposure to instruments where their edge does not exist for reasons that are almost always psychological rather than analytical. Familiarity with an instrument, the belief that the edge will return, the reluctance to admit that time spent developing a feel for that market has not produced a tradeable result, and the general human resistance to narrowing focus rather than broadening it all contribute to the persistence of exposure to instruments that the journal data has already identified as outside the trader’s genuine edge. Acting on what the data shows in this area requires a clarity and honesty that many traders find uncomfortable, but the performance improvement that comes from concentrating activity on instruments where a genuine edge exists is among the most reliable benefits that journal-driven strategy refinement produces.

The process of implementing session and instrument exposure adjustments should be gradual rather than simultaneous, and this is a practical requirement rather than a suggestion. Making multiple exposure adjustments at the same time makes it impossible to isolate the impact of each individual change through the ongoing review process. If a trader simultaneously eliminates one session, reduces size during another, cuts two instruments, and increases focus on a third, and performance improves over the following two months, there is no way to determine which of those changes drove the improvement or whether all of them were necessary. Making one adjustment at a time, tracking its impact across a sufficient sample before making the next adjustment, and building the changes sequentially rather than all at once produces a strategy refinement process whose outcomes are legible and whose individual contributions to performance improvement can be attributed to specific decisions rather than to the combined effect of multiple simultaneous changes whose individual impacts remain unknown.

How to Use Backtesting to Validate Journal-Driven Modifications

Journal analysis and backtesting serve complementary but distinct functions in the strategy refinement process, and understanding the relationship between them is what prevents journal-driven modifications from being applied prematurely in ways that introduce new problems rather than solving existing ones. Journal analysis identifies what to change. It reveals which setups are underperforming, which rules are being broken and at what cost, and which aspects of the strategy are not producing the results the underlying edge should generate. Backtesting answers the question that journal analysis cannot: whether the proposed change actually improves expectancy across a broader historical sample that extends beyond the period the journal covers and the specific market conditions that period contained.

The reason backtesting is a necessary step before implementing significant journal-driven modifications rather than an optional one is straightforward. A journal covers a finite period of trading history under a specific set of market conditions. The insights it produces are real and valuable, but they reflect what happened during that period rather than what will happen across the full range of conditions the strategy will eventually face. A modification that looks like an improvement based on six months of journal data may perform differently under market conditions that were not present during that six months. Backtesting against a longer historical sample that includes a variety of market regimes gives the modification a more demanding test than the journal period alone provides and surfaces problems with the proposed change that a limited sample would miss.

Structuring a backtest around a specific journal-identified modification requires translating the modification into a precise and testable rule before the backtest begins. This is the step that most traders skip or execute poorly, and it is the step that determines whether the backtest produces useful information or simply confirms whatever the trader expected to find. If the journal analysis has identified that a specific setup’s entry criteria should be tightened to require an additional confirmation before a position is opened, the backtest should test that exact rule change in isolation against the same setup applied without the additional confirmation requirement across the same historical sample. The comparison between the two versions of the rule across the same data is what tells the trader whether the modification improves expectancy or whether it simply filters out trades randomly without producing a meaningful change in the setup’s statistical profile.

The historical sample used for backtesting a journal-driven modification should be meaningfully larger than the journal period that identified the need for the change and should include market conditions that differ from those present during the journal review period. A backtest conducted only over the same period covered by the journal is not a validation. It is a restatement of the journal analysis using a different method. A meaningful backtest sample for most retail trading setups includes a minimum of one hundred instances of the setup across a period that contains both trending and ranging conditions, varying volatility regimes, and ideally multiple years of data rather than a single year that may represent a specific and non-representative market environment. The larger and more varied the backtest sample, the more confidence the result provides about whether the modification is genuinely improving expectancy or simply performing better during the specific conditions of a limited test period.

The risk of over-optimising based on a limited historical period is the most significant danger in the backtesting step of strategy refinement and the one that produces the most damaging outcomes when it is not recognised and managed. Over-optimisation occurs when a modification is adjusted and re-adjusted based on backtest results until it performs well on the historical data used for testing, at which point it has been calibrated to the specific characteristics of that data rather than to the underlying market dynamics the strategy is designed to exploit. A modification that has been optimised to perform well on a specific historical dataset will almost always perform worse in live trading than the backtest suggested because the specific characteristics of the historical data it was calibrated to are not replicated exactly in future market conditions. The protection against over-optimisation is testing modifications with the minimum number of adjustments necessary to address the specific weakness identified by the journal rather than iterating through multiple versions of the rule until the backtest result looks satisfactory.

Platforms like SuperTrader include backtesting tools that allow traders to validate journal-driven modifications without needing a separate dedicated backtesting platform. This integration between the journal layer and the backtesting layer is practically significant because it keeps the refinement process within a single environment where the journal data that identified the modification and the backtest that validates it are directly connected rather than conducted in separate tools with separate data sets. For traders who are working through the strategy refinement process outlined in this guide, the ability to move from journal insight to backtest validation within the same platform reduces the friction that causes many traders to skip the backtesting step entirely and apply modifications directly to their live trading before they have been adequately tested. A full review of SuperTrader’s backtesting capability and how it integrates with the journal and AI analysis features is available here.

How to Implement Strategy Changes Without Disrupting Your Edge

Identifying the right strategy modifications through journal analysis and validating them through backtesting are the analytical steps in the refinement process. Implementing those modifications in live trading without disrupting the edge that the existing strategy is producing is the execution step, and it is where many traders who have done the analytical work correctly undo its value by applying changes in a way that makes their impact impossible to measure and their contribution to performance improvement impossible to attribute.

The first and most important rule of strategy modification implementation is making one change at a time. This rule feels obvious when stated directly but is routinely violated in practice because journal analysis typically identifies multiple areas for improvement simultaneously and the temptation to address all of them at once is strong. A trader who has identified through quarterly review that one setup should be cut, that session exposure should be adjusted, that entry criteria on a second setup should be tightened, and that position sizing should be increased on a third setup has identified four separate modifications that each deserve to be implemented, tracked, and evaluated independently. Implementing all four simultaneously produces a strategy that is different in four ways from the one that generated the journal data, and any change in performance that follows cannot be attributed to any specific modification because the contribution of each individual change is indistinguishable from the combined effect of all four. Making one change, tracking its impact across a sufficient sample, and then making the next change produces a refinement process whose outcomes are legible and whose individual decisions can be evaluated and learned from.

The second requirement is defining in advance what success looks like for each modification and over what time period that success will be evaluated. A modification implemented without a predefined success criterion will be evaluated through the lens of recent results rather than against a clear standard, which means it will be judged as successful during good periods and unsuccessful during bad ones regardless of whether it is actually producing the expected improvement. Before implementing any modification, write down specifically what improvement the change is expected to produce, which metric or metrics will be used to measure that improvement, and across how many trades or what time period the evaluation will be conducted before a conclusion is drawn. A tightened entry criterion might be defined as successful if it improves the setup’s win rate by a minimum of five percentage points across the next one hundred trades without meaningfully reducing the average R-multiple. That definition is specific enough to evaluate objectively and concrete enough to prevent the assessment from being influenced by how recent results feel.

The third requirement is tracking the impact of each modification through the ongoing journal review process rather than evaluating it through overall performance alone. Overall performance is too noisy a signal to detect the impact of a single setup-level or rule-level modification, particularly over short periods where variance can easily mask a genuine improvement or create the appearance of improvement where none exists. The modification needs to be tracked at the level at which it was made. A change to the entry criteria of a specific setup should be tracked through the performance metrics of that specific setup across the trades taken since the change was implemented. A session-based sizing adjustment should be tracked through the risk-adjusted performance during that session across the period since the adjustment was made. Tracking at the right level of granularity is what allows the evaluation to detect the signal the modification is expected to produce rather than losing it in the noise of overall performance variation.

The fourth requirement is reverting changes that do not produce the expected improvement within the defined evaluation period. This is the step that requires the most discipline because it means accepting that a modification that seemed well-supported by the journal analysis and the backtest has not produced the expected result in live trading, and responding to that conclusion by removing the change rather than extending the evaluation period indefinitely in the hope that the result will eventually improve. A modification that has been evaluated across a sufficient sample and has not produced the improvement it was expected to produce is not a modification that needs more time. It is a modification that was either based on a pattern that does not generalise beyond the specific conditions of the journal and backtest periods, or that addressed a symptom rather than the underlying cause of the performance issue it was designed to solve. Reverting the change and returning to the analysis to identify a more precisely targeted modification is the correct response, and treating it as such rather than as a failure preserves both the integrity of the strategy and the validity of the refinement process.

The underlying principle that connects all four of these requirements is that strategy refinement should produce a strategy that is measurably better in specific and attributable ways rather than simply different in ways whose impact on performance cannot be determined. A trader who implements modifications one at a time, defines success criteria in advance, tracks impact at the right level of granularity, and reverts changes that do not meet their criteria is building a refinement process that compounds in effectiveness over time because every decision it produces is based on clear evidence and every outcome it generates feeds back into the next round of analysis with enough clarity to inform the next modification. A trader who implements multiple changes simultaneously, evaluates them through overall performance, and persists with modifications that are not working because the analysis said they should is running a process that generates activity without generating insight, which is the most expensive way to leave a trading strategy essentially unchanged while believing it is being systematically improved.

Building a Strategy Refinement Cycle

Strategy refinement that happens only in response to poor performance is not a refinement process. It is a crisis response dressed up as analysis, and it shares all the characteristics of reactive decision-making that the data-driven approach to strategy development is designed to replace. The difference between a trader whose strategy compounds in effectiveness over time and a trader whose strategy oscillates between versions of itself without ever becoming meaningfully better is almost always whether strategy refinement is embedded into a fixed and recurring routine or conducted occasionally when results deteriorate enough to demand attention.

Embedding strategy refinement into the regular self-analysis routine begins with linking quarterly behavioural audits directly to strategy review sessions. The quarterly audit, as outlined in the Trading Self-Analysis Guide, is the level of review at which the patterns that justify strategy modifications become most clearly visible. Session-specific underperformance that looked like variance at the weekly level and like a short-term pattern at the monthly level becomes a durable signal at the quarterly level when it has persisted across three months of varying market conditions. Setup-specific expectancy that was ambiguous across fifty trades becomes much clearer across one hundred and fifty. The mistake tag analysis that quantifies the financial cost of recurring errors across a quarter produces numbers large enough to justify specific rule changes in a way that the same analysis conducted over a single month does not.

Structuring the quarterly audit to flow directly into a strategy review session rather than treating them as separate activities is what makes the refinement cycle function as a continuous process rather than two disconnected activities. The audit identifies the patterns. The strategy review session translates those patterns into specific proposed modifications, evaluates each modification against the data requirements covered earlier in this guide, and produces a defined list of changes to be implemented, backtested, or monitored over the following quarter. The output of every quarterly audit should be a written record of the strategy modifications being considered, the data supporting each one, the success criteria that will be used to evaluate each modification, and the timeline over which each evaluation will be conducted. That written record becomes the agenda for the following quarter’s audit, creating a direct and structured link between each review cycle and the one that follows it.

Setting a defined cadence for evaluating and updating the trading plan based on journal data is the structural commitment that keeps the refinement cycle running on schedule rather than slipping into the reactive pattern it is designed to replace. The cadence should be fixed and calendar-based rather than performance-triggered. A strategy review conducted at the end of every quarter regardless of whether recent results have been good or bad is a fundamentally different process from a strategy review conducted when results deteriorate enough to demand one, even if the analytical content of the two sessions is identical. The fixed cadence removes the emotional trigger from the timing of the review, which means the review is conducted with the same analytical objectivity during good periods as during bad ones and produces conclusions that reflect the full picture of what the data shows rather than the subset of the data that is most salient when recent results are painful.

The trading plan itself should be treated as a document that is reviewed and updated on a fixed schedule rather than a static reference document that is consulted occasionally and modified reactively. A practical approach is to maintain the trading plan as a versioned document with a clear record of every modification made, the date it was implemented, the journal data that supported it, and the outcome of the evaluation period that followed. This version history serves two purposes. It creates accountability to the refinement process by making every modification a documented decision with a defined rationale rather than an informal adjustment that can be reversed or forgotten without consequence. And it creates a longitudinal record of how the strategy has evolved over time that is itself a source of insight, revealing which types of modifications have historically produced improvement and which have not, and informing the judgement applied to future refinement decisions with evidence from the full history of the trader’s own strategy development process rather than from the most recent quarter alone.

The cadence of the refinement cycle should also include a mid-quarter checkpoint that sits between the monthly performance review and the quarterly audit. This checkpoint is not a full strategy review but a brief assessment of whether the modifications implemented at the start of the quarter are tracking toward the success criteria defined for them or whether early signals suggest that a modification is not producing the expected improvement and may need to be reverted before the full evaluation period has elapsed. Catching a modification that is clearly not working at the mid-quarter checkpoint rather than waiting for the full quarterly audit to confirm it limits the number of trades conducted under a rule that is not improving performance and preserves the integrity of the journal data that the next quarterly analysis will be based on.

The traders who build the most effective strategy refinement cycles are not necessarily the ones who make the most modifications or conduct the most sophisticated analysis. They are the ones who review consistently, modify deliberately, track carefully, and treat the refinement process itself as a discipline that requires the same commitment to process over outcome that good trading requires. A refinement cycle applied consistently over two or three years produces a strategy that is meaningfully better calibrated to the trader’s actual edge, their psychological profile, their best sessions and instruments, and the market conditions they trade in than any strategy that was written once and left largely unchanged across the same period. That compounding improvement over time is the return on the investment of building and maintaining the cycle, and it is available to any trader who is willing to treat strategy refinement as a non-negotiable part of the trading process rather than an occasional response to pain.

The Role of Journal Tools in Strategy Refinement

The strategy refinement process outlined in this guide can be conducted using any journal tool that captures the right data consistently, including a well-structured spreadsheet. The framework, the metrics, and the decision-making logic are what drive the quality of the refinement process, and no platform compensates for the absence of the analytical discipline and consistency that the process requires. That said, the right journal platform makes strategy refinement significantly more accessible, more data-driven, and more likely to surface the specific insights that justify modification decisions, and the difference between platforms becomes most apparent at exactly the point where refinement analysis is being conducted.

The primary way that journal platforms improve the strategy refinement process is by reducing the analytical burden involved in preparing the data for review. Segmenting trade history by setup, session, instrument, and mental state across hundreds of trades, calculating the relevant metrics for each segment independently, and presenting the results in a format that makes patterns visible without requiring manual calculation is work that a capable journal platform handles automatically. When the data is already organised and the metrics are already calculated, the refinement session can focus on interpretation and decision-making rather than on data preparation, which produces better analytical outcomes and makes the process sustainable over the long term.

Platforms like SuperTrader go further by automating much of the pattern recognition process that underpins refinement decisions through AI-driven insights. Rather than requiring the trader to segment the data manually and know what patterns to look for, SuperTrader’s AI Mentor analyses the full trade history and surfaces behavioural leaks, setup-specific performance variation, and session and instrument patterns that the trader may not have identified through manual review. For traders who want the benefits of data-driven strategy refinement without building the full analytical infrastructure to conduct it manually, this automated insight layer significantly lowers the barrier to acting on what the journal data is showing. SuperTrader also includes backtesting tools that allow traders to validate proposed modifications within the same platform rather than requiring a separate backtesting environment, which keeps the full refinement cycle from journal insight through backtest validation within a single integrated workflow. A full independent review of SuperTrader is available at TradingJournalReviews.com.

For traders who have the quantitative mindset and the analytical inclination to conduct their own granular setup and session analysis, TradesViz provides the custom reporting tools and multi-dimensional filtering capabilities that make that level of analysis practical rather than prohibitively time-consuming. The ability to build custom dashboards that reflect a trader’s own analytical priorities, apply filters across multiple variables simultaneously, and generate reports that isolate the performance of specific setups under specific conditions gives quantitatively minded traders a level of analytical control over their refinement process that more standardised reporting environments do not provide. When the strategy refinement questions being asked are highly specific, such as how a particular setup performs during a specific session on a specific instrument under a specific volatility condition, TradesViz’s filtering infrastructure is built to answer those questions from real trade data in a way that most competing platforms are not. A full independent review of TradesViz is available here.

TradeZella’s playbook feature occupies a particularly useful position in the strategy refinement context because it is specifically designed to track setup-specific performance over time in a structured and consistent way. The ability to create named playbook entries for each setup in the trading plan and tag every trade to one of those entries means that the setup-level performance data needed for refinement decisions is always organised and always current without requiring any additional effort at the point of review. When a quarterly strategy review session requires the win rate, average R-multiple, and Profit Factor for each individual setup across the quarter’s trades, a trader using TradeZella’s playbook feature has that data immediately available in the format needed for refinement analysis rather than having to construct it from raw trade records. For traders whose primary refinement focus is setup selection and setup-level rule modification, TradeZella’s playbook infrastructure directly supports the most important layer of the refinement process. A full independent review of TradeZella is available at TradingJournalReviews.com.

The practical implication for traders choosing a journal platform with strategy refinement in mind is that the platform should match the type of refinement analysis they intend to conduct most frequently. A trader whose refinement process is primarily focused on behavioural pattern recognition and automated insight generation will get the most from SuperTrader. A trader whose refinement process involves granular multi-variable analysis built around their own analytical framework will get the most from TradesViz. A trader whose refinement process centres on setup-specific performance tracking and playbook-level statistical analysis will get the most from TradeZella. For a full comparison of these platforms and others across features, pricing, integrations, and strategy refinement capability, visit TradingJournalReviews.com where each platform is assessed independently so you can match the right tool to the specific refinement process you are building.

Frequently Asked Questions

How do I know when to cut a setup from my trading plan?

The decision to cut a setup should be driven by three specific data signals rather than by recent results or frustration with a period of underperformance. The first signal is negative expectancy across a minimum of fifty trades in that setup, meaning the setup is losing money on average at a rate that cannot be explained by normal variance across a sample of that size. The second signal is a consistently poor R-multiple profile despite an acceptable win rate, which indicates that the setup is winning often enough to feel viable but giving back more on each loss than it makes on each winner in a way that produces negative expectancy regardless of how the win rate looks. The third signal is a setup that only produces positive results under specific market conditions that are not reliably or frequently present. When one or more of these signals is present across a sufficient sample, the data is providing a clear argument for cutting the setup and the decision should be made on that basis rather than deferred in the hope that results will improve without a specific reason to expect they will.

How many trades do I need before refining a setup?

A minimum of fifty trades in a specific setup is the threshold below which setup-level conclusions are too heavily influenced by variance to be acted on reliably. One hundred trades or more is a more robust sample for modifications that involve significant changes such as cutting a setup entirely or meaningfully increasing size on it. Below fifty trades, the sample is too small to distinguish a genuine performance signal from a run of good or bad luck, and modifications made on that basis are reactions to noise rather than responses to a real pattern in the data. This does not mean that obvious execution problems identified through the weekly trade review process should be ignored until fifty trades have been logged. Process-level observations about rule deviations and execution quality are valid from the first trade. The fifty trade threshold applies specifically to the statistical conclusions about setup expectancy that justify structural modifications to the trading plan.

Should I backtest every strategy change identified through my journal?

Every modification that involves a structural change to a setup’s rules, a significant adjustment to position sizing, or a meaningful change to session or instrument exposure should be backtested before being implemented at full scale in live trading. Backtesting is the step that distinguishes between a modification that is supported by journal data from a specific period and a modification that holds up across a broader historical sample under varying market conditions. Minor process adjustments such as changing the order in which pre-trade checklist items are reviewed or adjusting the format of journal entries do not require backtesting because they do not affect the strategy’s expectancy directly. Any change that does affect expectancy directly should be validated through backtesting before live implementation, not because the journal analysis that identified the need for the change is unreliable, but because the journal covers a finite and specific period whose conditions may not be fully representative of the range of conditions the modified strategy will eventually face.

How often should I review and update my trading strategy?

The trading strategy should be formally reviewed at the end of every quarter as part of the quarterly behavioural audit described in the Trading Self-Analysis Guide. This quarterly review is when the data sample is large enough to support structural conclusions about setup performance, session exposure, and instrument selection that the weekly and monthly reviews are not designed to produce. Between quarterly reviews, a mid-quarter checkpoint should assess whether modifications implemented at the start of the quarter are tracking toward their defined success criteria. The trading plan document itself should be updated only when a modification has been validated through backtesting and implemented in live trading, not at the point of identifying a potential modification that has not yet been tested. Updating the plan before a modification has been validated treats a hypothesis as a conclusion, which introduces changes into the written strategy that may not survive the backtesting and evaluation process.

What is the difference between strategy refinement and strategy abandonment?

Strategy refinement is the process of making specific, data-supported modifications to individual components of an existing strategy while preserving the core logic and edge that the strategy is built around. It changes entry criteria, adjusts position sizing, modifies exit rules, or restructures session exposure in ways that are targeted at specific identified weaknesses without replacing the fundamental approach that produced the edge the journal data has confirmed exists. Strategy abandonment is the wholesale replacement of a strategy with a different approach, typically triggered by a period of poor performance rather than by data that shows the existing edge has genuinely deteriorated. The most reliable way to distinguish between the two in practice is to ask whether the proposed changes are supported by specific data signals that point to specific weaknesses in the current approach or whether they are driven primarily by frustration with recent results and a desire to do something different. Data-supported targeted modifications are refinement. Wholesale changes made in response to emotional pressure are abandonment, regardless of how they are framed.

Can I refine my strategy without a dedicated journal platform?

Yes, and many traders have built effective strategy refinement processes using well-structured spreadsheets rather than dedicated journal platforms. The framework, the metrics, and the analytical discipline are what drive the quality of the refinement process, and a spreadsheet that captures trade data with the right variables and calculates the right metrics by setup, session, and instrument can support every layer of the refinement process described in this guide. The practical limitation of a spreadsheet-based approach is the time and effort required to prepare the data for each review session, which increases the friction in the process and makes it less likely to be conducted consistently over the long term. Dedicated journal platforms reduce that friction by handling data organisation and metric calculation automatically, which makes the review process faster and more sustainable. For traders who are evaluating platform options with strategy refinement in mind, full independent reviews of the leading journal platforms are available at TradingJournalReviews.com.

How do I avoid over-optimising my strategy based on journal data?

Over-optimisation occurs when modifications are adjusted and re-adjusted until they perform well on a specific historical dataset rather than being calibrated to the underlying market dynamics the strategy is designed to exploit. The primary protection against it is testing modifications with the minimum number of adjustments necessary to address the specific weakness identified by the journal rather than iterating through multiple versions of a rule until the backtest result looks satisfactory. A second protection is using a backtest sample that is significantly larger and more varied than the journal period that identified the need for the change, which prevents modifications from being calibrated to the specific conditions of a limited period. A third protection is making one modification at a time and evaluating its impact across a sufficient live trading sample before making further adjustments, which prevents the accumulation of multiple small optimisations that collectively produce a strategy that performs well on historical data and poorly in live trading conditions that differ from the historical sample in ways that were not anticipated.

What metrics matter most when refining a trading setup?

The three metrics that matter most for setup refinement decisions are win rate by setup, average R-multiple by setup, and Profit Factor by setup, each calculated independently across a sufficient sample rather than in aggregate with other setups. Win rate tells you how often the setup produces a winner. Average R-multiple tells you the ratio of average winning trade size to average losing trade size in risk-adjusted terms, which is the metric most directly connected to expectancy. Profit Factor tells you the ratio of gross profit to gross loss across all trades in the setup, which gives a single number that reflects both win rate and R-multiple in a way that makes setups with different win rate and R-multiple profiles directly comparable. Beyond these three core metrics, holding time analysis is particularly useful for identifying exit rule problems, and the financial cost of mistake tags associated with a specific setup is useful for identifying process-level issues that are suppressing the setup’s performance below what the underlying edge should produce.